{kind=link}

Is Nvidia now the platform every AI company must buy into?

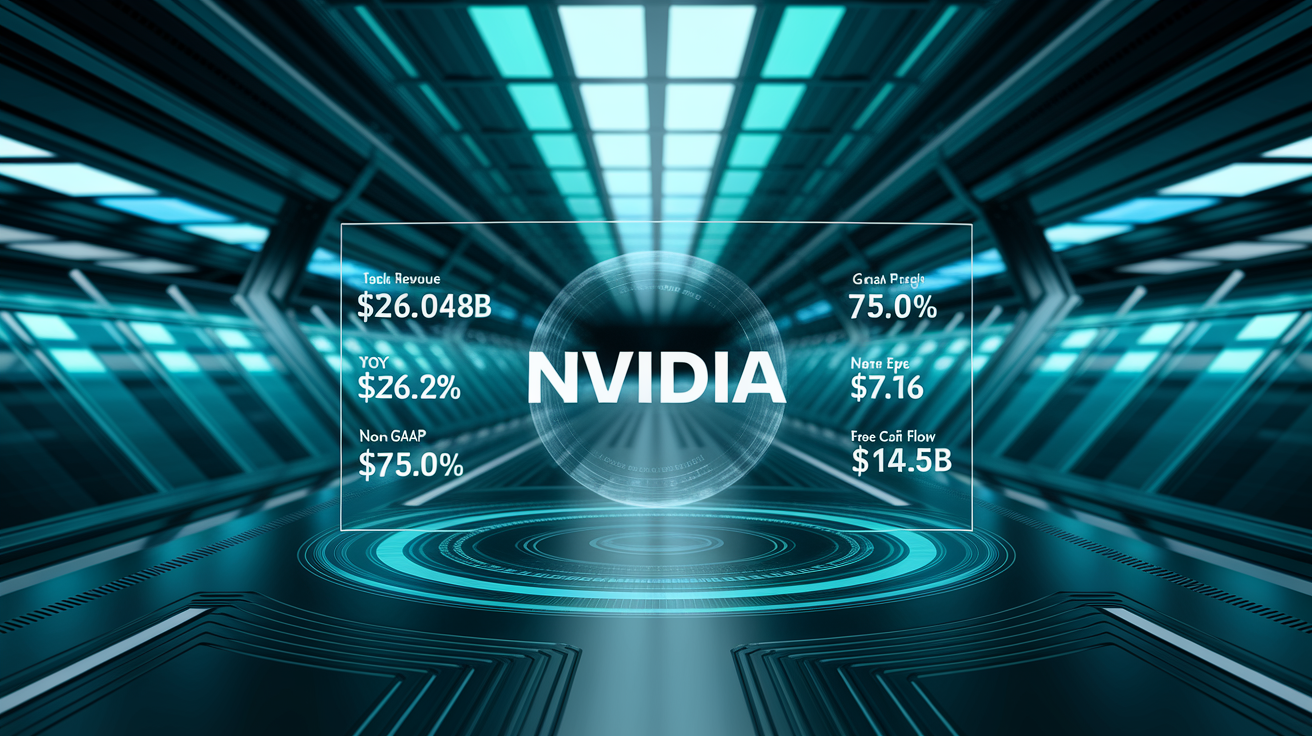

Last quarter it reported $26.04 billion in revenue, up 262 percent year over year, with data center sales of $22.6 billion making up 87 percent of the total.

That sharp shift shows AI chips are driving the results and squeezing other segments into the background.

In this breakdown we’ll explain why that matters for portfolios, what risks to watch, like supply and the Blackwell ramp, and how investors might position for a market where AI demand dominates.

Nvidia Earnings Overview: Key Numbers at a Glance

Nvidia just posted another absurd quarter of revenue growth, powered by AI chip demand that won’t quit. Total revenue hit $26.04 billion, up 262 percent year over year and 18 percent from the previous quarter. That kind of growth shows just how dominant the company is in data center accelerators, which now make up the bulk of sales. Non-GAAP earnings per share came in at $5.16, obliterating last year’s $0.40 and crushing what analysts expected.

Margins expanded hard as high margin AI chips took over a bigger slice of the revenue pie. Non-GAAP gross margin reached 75.0 percent, up from 70.1 percent a year ago. Operating margin climbed to 62 percent, which tells you everything about pricing power and operational leverage when data center revenue scales like this. Free cash flow surged to $14.5 billion for the quarter, giving Nvidia plenty of firepower to fund R&D, return cash to shareholders, and deal with any supply constraints.

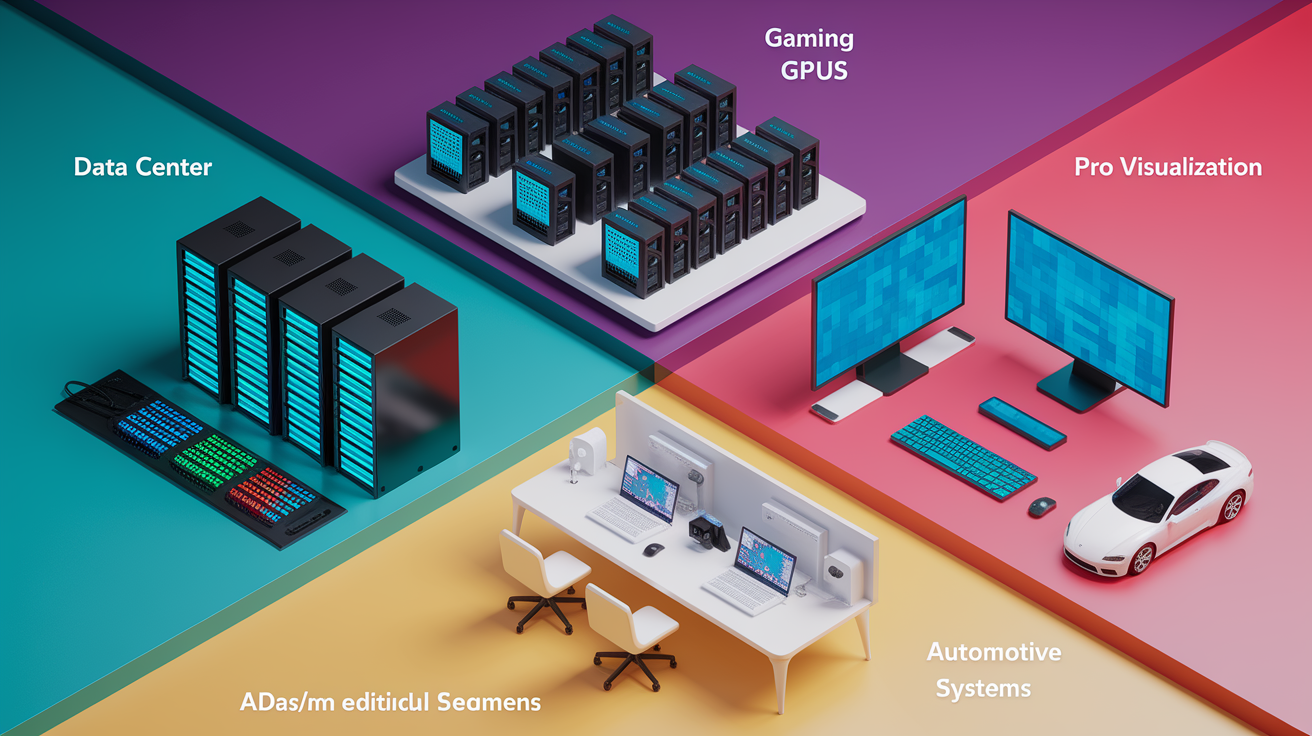

The real story is data center revenue, which hit $22.6 billion and accounted for 87 percent of total revenue. Gaming brought in $2.9 billion, professional visualization added $0.4 billion, and automotive plus other segments contributed roughly $0.3 billion each. Management called out strong sell-through for H100 and H200 chips, with enterprise and cloud customers ramping up deployments to handle generative AI workloads.

Here’s what matters most:

- Total revenue of $26.04 billion, up 262 percent year over year

- Data center revenue of $22.6 billion, up 427 percent year over year

- Non-GAAP EPS of $5.16 versus $0.40 in the prior year quarter

- Non-GAAP gross margin of 75.0 percent, expanding 490 basis points year over year

- Free cash flow of $14.5 billion, reflecting strong operating leverage

Breakdown by Business Segment

Data center revenue jumped to $22.6 billion, driven almost entirely by sales of Hopper architecture GPUs into AI training and inference infrastructure. Hyperscale cloud providers, consumer internet companies, and enterprise customers all ramped purchases to support large language models and AI powered applications. The segment grew 427 percent year over year and now represents 87 percent of total revenue. Management noted strong demand visibility extending multiple quarters, backed by multi-billion dollar supply agreements with major cloud vendors.

Gaming revenue reached $2.9 billion, up 56 percent year over year but flat sequentially. The recovery reflects steady GeForce RTX 40 series desktop GPU sales and improving channel inventory. Nvidia highlighted strong engagement with new game releases that use ray tracing and DLSS technology, though the segment remains far smaller than data center. Average selling prices held firm as the product mix shifted toward higher end SKUs, and unit volumes rose modestly as supply normalized.

Professional visualization revenue totaled $0.4 billion, up 108 percent year over year. The segment benefits from workstation refresh cycles and adoption of Omniverse for design, engineering, and digital twin applications. Growth here is slower and lumpier than data center, but margins stay attractive. Automotive revenue hit $0.3 billion, up 4 percent year over year, with most growth coming from advanced driver assistance platforms and in-vehicle infotainment solutions. This segment carries long development cycles and lower near term revenue contribution.

| Segment | Revenue | YoY Change | Key Driver |

|---|---|---|---|

| Data Center | $22.6 billion | +427% | AI training and inference demand (H100/H200) |

| Gaming | $2.9 billion | +56% | RTX 40-series desktop GPU sales, stable ASPs |

| Pro Visualization | $0.4 billion | +108% | Workstation refresh, Omniverse adoption |

| Automotive | $0.3 billion | +4% | ADAS platforms, in-vehicle infotainment |

Comparison Against Analyst Expectations

Nvidia beat consensus estimates across the board. Wall Street had forecast revenue of $24.6 billion, so the reported $26.04 billion represented a beat of $1.44 billion, or roughly 6 percent. Non-GAAP EPS of $5.16 sailed past the consensus estimate of $4.64, a beat of $0.52 per share, or 11 percent. Both top line and bottom line outperformance show that Nvidia is capturing AI demand faster than most analysts modeled, and that pricing power isn’t going anywhere.

The upside surprise extended to segment detail. Data center revenue came in above most buy side models, which had penciled in around $21 billion. Gaming revenue also edged past expectations, as many analysts assumed flat to slightly down sequential performance given typical seasonality. Gross margin of 75.0 percent topped the Street’s 74.2 percent forecast, driven by a richer product mix and lower than expected cost of goods sold as manufacturing yields improved.

Most significant beats:

- Revenue beat of $1.44 billion, or 6 percent above consensus $24.6 billion

- Non-GAAP EPS beat of $0.52, or 11 percent above consensus $4.64

- Gross margin of 75.0 percent versus consensus 74.2 percent, reflecting stronger mix and yields

Management Commentary and Strategic Highlights

CEO Jensen Huang emphasized that demand for AI infrastructure shows no sign of slowing. He noted that enterprise adoption is accelerating as companies move generative AI projects from pilot to production, driving multi year upgrade cycles across data centers. Huang also highlighted Nvidia’s software ecosystem, including CUDA, TensorRT, and NIM microservices, as a key moat that keeps customers locked into the platform even as competition emerges. He called the current wave “the beginning of a new computing era,” with AI workloads fundamentally reshaping data center architecture.

The company addressed supply constraints, stating that manufacturing capacity has expanded significantly through partnerships with TSMC and other foundries. Management expects to meet demand for the new Blackwell architecture in the second half of the calendar year, with initial customer shipments already underway. Huang also previewed momentum in AI inference, a segment that’s expected to grow rapidly as deployed models scale and enterprises run billions of daily queries.

Strategic priorities center on maintaining technology leadership and broadening the addressable market. Nvidia is investing heavily in custom silicon for large cloud providers, networking infrastructure through the Spectrum-X platform, and software solutions that monetize the installed base. Management framed the opportunity as a multi trillion dollar total addressable market spanning training, inference, edge AI, and sovereign AI clouds built by governments and telecom operators.

Key Executive Quotes

“We’re seeing customers shift from proof of concept to full scale production deployments, and that transition is driving sustained multi quarter demand visibility.”

“Blackwell is ramping on schedule, and early feedback from partners confirms that performance and efficiency gains are exceeding expectations, positioning us well for the next product cycle.”

Forward Guidance and Outlook

Nvidia guided next quarter revenue to $37.5 billion, plus or minus 2 percent, implying continued strong sequential and year over year growth. That midpoint implies roughly 44 percent sequential growth and would put the company on track for over $100 billion in annual revenue. The guidance reflects robust bookings for Hopper and early Blackwell ramps, as well as stable gaming and professional visualization trends. Management noted that visibility remains strong due to long lead supply commitments from hyperscale and enterprise customers.

Gross margin guidance for the next quarter is approximately 73.5 percent on a non-GAAP basis, slightly below the current quarter due to the initial Blackwell mix and ramp costs. Operating expenses are expected to rise as the company scales engineering headcount and invests in next generation architecture. Management emphasized that margin compression will be temporary, with gross margins expected to re-accelerate as Blackwell production scales and yields improve.

Capital expenditure is projected to increase modestly to support lab infrastructure, test capacity, and data center build outs for internal AI research. Free cash flow generation is expected to remain robust, funding a combination of share buybacks and dividend growth. The company authorized an additional $50 billion in share repurchases, signaling confidence in sustained profitability and cash generation.

Key guidance figures:

- Next quarter revenue of $37.5 billion, plus or minus 2 percent, up roughly 44 percent sequentially

- Non-GAAP gross margin of approximately 73.5 percent, reflecting early Blackwell ramp dynamics

- Operating expenses rising in line with headcount growth and R&D investments

- Continued strong free cash flow supporting $50 billion incremental share buyback authorization

Market Reaction and Stock Performance

Nvidia shares jumped 9 percent in after hours trading immediately following the earnings release, adding roughly $250 billion in market capitalization. The move reflected investor relief that both revenue and guidance exceeded high expectations, and that management remains confident in multi quarter demand visibility. Intraday volatility was elevated, with the stock trading in a $15 range as algorithmic traders digested the report and options positioning adjusted.

The rally extended into the next trading session, with shares opening up 7 percent and holding gains through the close. Volume surged to more than three times the 30 day average, indicating broad institutional participation. The semiconductor index also rose, though Nvidia’s outperformance was clear. Options markets showed heavy call buying, with implied volatility declining post earnings as uncertainty around the quarter resolved favorably.

Market sentiment indicators:

- After hours gain of 9 percent, adding approximately $250 billion in market cap

- Next day open up 7 percent, sustained through the session on triple average volume

- Heavy call option activity and declining implied volatility signaling reduced uncertainty

Key Takeaways for Investors

Nvidia’s results confirm that AI infrastructure spending remains in full expansion mode, with no visible slowdown in enterprise or cloud demand. The company’s ability to beat high expectations and raise guidance demonstrates pricing power, execution strength, and a widening competitive moat. Data center concentration now exceeds 85 percent of revenue, which magnifies growth but also introduces cyclical risk if AI capital spending moderates.

Long term investors should watch for signs that inference workloads are scaling, as that segment offers a second wave of growth beyond the current training focused demand. The Blackwell ramp and gross margin trajectory in the coming quarters will be critical indicators of manufacturing execution and competitive positioning. Supply chain diversity and customer concentration remain top risks, particularly if any hyperscale customer reduces orders or if geopolitical tensions disrupt foundry access.

Key investor takeaways:

- AI chip demand continues to exceed supply, supporting sustained revenue growth and margin expansion

- Blackwell architecture is ramping on schedule, with strong early customer feedback and multi quarter visibility

- Data center now represents 87 percent of revenue, creating upside leverage but also cyclical concentration risk

- Free cash flow generation and $50 billion buyback authorization signal management confidence in durable profitability

Final Words

in the action Nvidia posted robust revenue and EPS, led by data-center AI chip demand and firmer margins.

That matters because stronger cash flow and clearer guidance shift the debate from “if” to “how fast.” Watch data-center growth, margins, guidance, and supply signals for confirmation.

This nvidia earnings report breakdown highlights where the opportunities and risks sit. Stay diversified, size positions thoughtfully, and take a cautiously optimistic view of the AI-driven runway.

FAQ

Q: How did Nvidia do on their earnings report?

A: The Nvidia earnings report showed robust results, with revenue and EPS beating consensus, driven by data-center AI demand, margin expansion, and upbeat guidance that reinforced its growth narrative for investors.

Q: What did Jim Cramer say about Nvidia?

A: Jim Cramer said Nvidia is a leading AI play and praised its strong fundamentals, while warning investors to watch valuation and potential volatility as part of a balanced, long-term approach.

Q: Are 75% Nvidia employees millionaires?

A: The claim that 75% of Nvidia employees are millionaires is overstated; many staff have equity, but the true share depends on tenure, role, option timing, and vesting, not a uniform 75 percent.

Q: What if I invested $10,000 in Nvidia 5 years ago?

A: Investing $10,000 in Nvidia five years ago would now be worth the number of shares bought times today’s price; calculate by dividing $10,000 by the purchase price, then multiplying by current price.